On-line Session For Steps To Win the Interim Maintenance

&

On-line Session For Stress Management Through Meditation

Online Registration

in case in issue please contact helpdv@yahoo.in

| K.L. Bablani. on TEP and RTI Tax Evasion Petiti… | |

| Sucharita on Application Format For Mutual… | |

| Shaun Peter Phillips on 5 Steps To Win The Interim… | |

| NALMALA KRISHNARAO on DV Act Expert Group on WhatsAp… | |

| preeti on Application Format For Mutual… |

On-line Session For Steps To Win the Interim Maintenance

&

On-line Session For Stress Management Through Meditation

Online Registration

in case in issue please contact helpdv@yahoo.in

The WordPress.com stats helper monkeys prepared a 2014 annual report for this blog.

Here’s an excerpt:

The concert hall at the Sydney Opera House holds 2,700 people. This blog was viewed about 26,000 times in 2014. If it were a concert at Sydney Opera House, it would take about 10 sold-out performances for that many people to see it.

Frequently Asked Questions on TEP (Tax Evasion Petition)

1. What is Mean by TEP

Tax Evasion Petition: A complain letter to Income tax Department (CBDT) with proof to investigate the revenue loss to government ex-checker because of such evasion

2. Why TEP

Mostly wife always give the list of stridhan 3-4 times from the actual list of stridhan / huge amount of dowry in her compliant. So we have the legal tool for this we should complaint in the Income Tax dept. for verifying that they’ve declared that much income or not. If they’ve not declared that much income then recover the tax with some penalty. But very few people go to Income Tax Dept to ask for verifying their income.

3. When to file TEP

a. If your wife do the false allegation in DV affidavit case or in 498a FIR and about huge amount of money spend in Marriage and stridhan or dowry or exchange of money in your marriage.

b. If your Father in Law has disproportionate assets w.r.t his income, TEP is possible, You have to show undisclosed income, unaccounted flow of cash, unexplained expenditure etc. to file TEP.

c. If the value of the furniture, gold, cash was not proportionate to his income at the time of expenditure, you can file TEP.

4. What are the task before filing the TEP

a. Get the certified copy of the compliant

b. Get the PAN number if you know

c. Prepared the proper application

d. Get the address of Income tax department in Your area

5. What document required to file the TEP

a. TEP application- Format is available on blow link

b. DV case or Crpc 125 Case Affidavit or FIR copy of 498a or any authentic document as per evidence act where your wife told they spend huge money in Marriage / dowry / stridhan

6. What are the grounds for filling TEP?

If you have FIR copy/DV copy/Bills of marriage expenses claimed by opposite party wherein they have mentioned huge amount (Beyond their capacity to spend). Bills of marriage expenses claimed by opposite party if you have any detail wherein they have mentioned larger amount (Beyond their capacity to spend).Better to have more and more information like their bank accounts/properties also

7. I don’t have Pan number of Father-In-Law how to file the TEP

No need to PAN number to file the TEP just give the full name, address detail

8. How much time it has take to resolved the quarry under TEP

It take the time generally 1.5 year to 3 year depending upon your follow up / RTI

9. What are the Advantages of TEP

a. For sure this will go against the 498A / DV family as it will expose their false allegations

b. You can screw the 498a family royally, with this “Legal Cruelty” tool.

c. Can handle without legal aid. No lawyer expanse

d. Fire numerous RTIs based on the opponents’ profile and fast track the TEP investigation..

e. You can call the Investigation officer with Investigation report using witness summons in your CROSS stage then all the false of dowry will be nullified and their case is weak, you have upper hand.

10. What are the Disadvantages:

a. Will not work when less amount is claimed as dowry

b. Needs to cope up with time delay for RTI replies from govt. departments & information commission response for appeals.

c. Government machinery may not work with expected efficiency.

d. Very indirect method of attacking the opponents.

11. Where should I make a complaint?

To “The Chief Commissioner of Income Tax” of your particular state with a copy to DGIT(Investigations) Income Tax Department. Secondly to Member Investigation, CBDT, Department of Revenue, Ministry of Finance, North Block. New Delhi.

12. How TEP Strategy work

a. Ask for detailed Investigation report of the proven TEP.

b. Submit the same in the 498A court questioning that with IT Deptt also not able to find the source of income to pay such a dowry, the case definitely is false as it has been investigated by a party having no interest (i.e. IT Deptt) and that too a Govt. department.

c. To submit to the 498A court that the family is itself dishonest by nature and hence has filed this 498A for encasings money using Law as an extortion tool.

13. Format of TEP Application

https://mensrightactivist.wordpress.com/category/templates/tep/

14. What will happen to 498a family if you are able to successful filed TEP

a. They need to pay the Tax of undisclosed income

b. They need to disclose the source of income from unaccounted amount

c. Plus penalty, which can not be less than 100% of the evaded amount and notmore than 300% of the evaded amount

d. You will get the 10% prize amount

15. Following precaution should be take care before filing the RTI on TEO

a. Your RTI application is proper and short

b. You should have provided grounds for disclosure of the said information by stating that the Truth and Justice are the superior most “Public Interest” subjects and the denial of information can hamper your liberty and Constitutional right under article 21 regarding Right to Live with Dignity.

c. You should file the multiple RTI with short question

d. While asking information under RTI Act care should be taken as there is no need to ask income tax return. Instead ask for whether the income shown is below or above the one claimed in your FIR or CAWCell complaint. Then it will be easier for them to reply as here you are not asking return, neither you are asking amount.You will get the information which will be sufficient.

e. Also do ask for how many times notices were sent, if one of the notice is not complied then it attracts penalties and so on.

16. How to get the output of TEP

Outcome of the TEP has to be disclosed as per the following decisions of the CIC:

Click to access cic_deci…17_M_54145.pdf

Click to access cic_decision…4032009-01.pdf

17. What is term Tax evader?

Tax evader is the person who has not submitted required Income tax as per law.

18. Step and Process of TEP

a. Filled TEP in Income Tax department

b. Sent RTI to find get status of TEP on November ,

c. If you get the negative response of the RTI “The CPIO denied the information requested, citing Section 8(1)(j) and 8(1)(h) of the RTI Act, 2005. ”

d. Sent first Appeal to concern office 2

e. You will get some response from of my first appeal and RTI as well and in the RTI response

f. Ask the detail report in your case using CRPC 91 or witness summons

g. Get the final report from the authority

19. Problem with TEP

a. One major hurdle is the statutory limitation of TEP of 6 years.

b. More than 6 years old, the department are allowed to not investigate apparently they carry the records only 6 years back – Hence filing TEP as soon as possible is best thingto do.

c. IT Returns can be opened for 4 years, if the amount realizable is less than 1 Lakh

d. IT Returns can be opened for 6 years, if the amount realizable is more than 1 Lakh

20. What are the different categories of TEP INVESTIGATION?

a. Z- Categories – All the personal complient are consider like TEP against 498a Family, this is slow and low priority

b. Y- Categories – All the business man with huge turn over this is medium priority

c. X- Categories – All Major fraud this is has the highest priority

21. What is the judgments refer by Income tax authorities to reject information under RTI Act 2005?

The Hon’ble Supreme Court in the case Girish Ramchandra Deshpande Vs. CIC dated October 3,2012 has held that the details disclosed by a person in his Income Tax Returns are “personal information” which stand exempted from disclosure u/s 8(1)(j) of the RTI Act unless a larger public interest is involved. In the instant case, the appellant has not been able to establish that the information sought for is for larger public interest. In fact, the appellant has sought this information on the ground that it was on the basis of his complaint that the IT authorities had ordered reassessment. In the light of the Supreme Court decision, the Commission concurs with the decision of the CPIO and Appellate Authority.(Ref. (Civil) No. 27734 of 2012 (@ CC 14781/2012)

22. CIC judgment which You should attach with First Appeal.

File No.CIC/DS/A/2011/003792/RM

“As the appellant has provided information relating to tax evasion, the CPIO is directed to inform the appellant as to whether the information provided by him was true or false and to disclose the broad outcome of the reassessment, without divulging specific details, once the process is completed.”

23. Where can I complaint if Income Tax officer is not taking proper action on TEP?

You can complaint to Vigilance department of Income Tax. Refer to below link for more detail http://www.incometaxindia.gov.in/vigilance/compl.html

24. How can I show larger public interest in my RTI against TEP?

Firstly, Tax Evasion is a crime and the knowledge is needed in public domain. (It is different than asking IT Returns). Secondly the information is required to prove innocence of few people (More than ONE)

25. What happen after filing TEP

Income tax department issue notice u/s 142(1) of income tax Act. The parties need to respond within one month otherwise there is a penalty of upto 10 000/- for disobeying notice. But no one cares as income tax officer never implement. The copy of the summon has a clause which reads as follows

“Without prejudice to the provisions of any other law for the time being in force, if you intentionally omit to so attend and give evidence or to produce the books of accounts and or documents a penalty for a sum which shall not be less than Rs.1000/- (Rupees one thousand) but which may extend to Rs. 10,000/- (Rupees ten thousand) for each default or failure shall be imposed upon you under section 272A(1)(e) of the Income-tax Act, 1961/37(2) of Wealth Tax act, 1957.”

If required ITO can issue summons u/s 131 of the Income Tax Act, 1961 wherein opposite party will be directed to present himself/herself before ITO

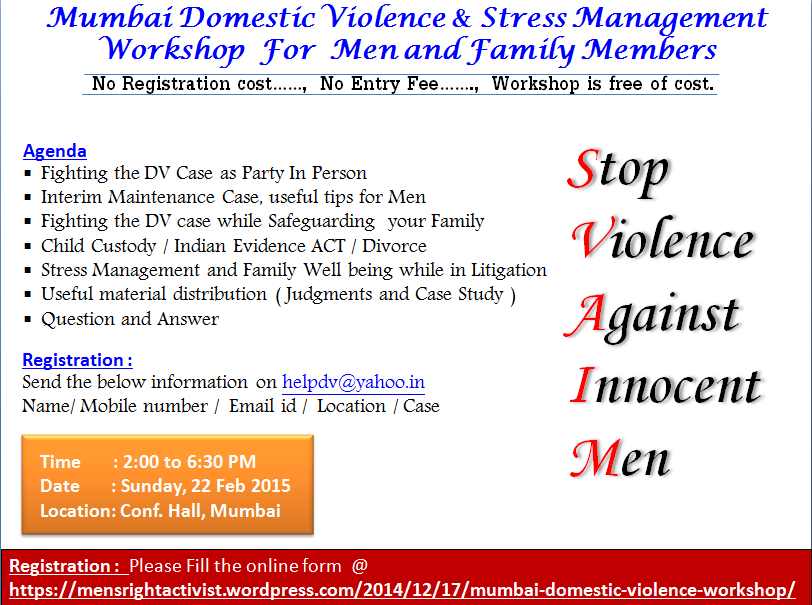

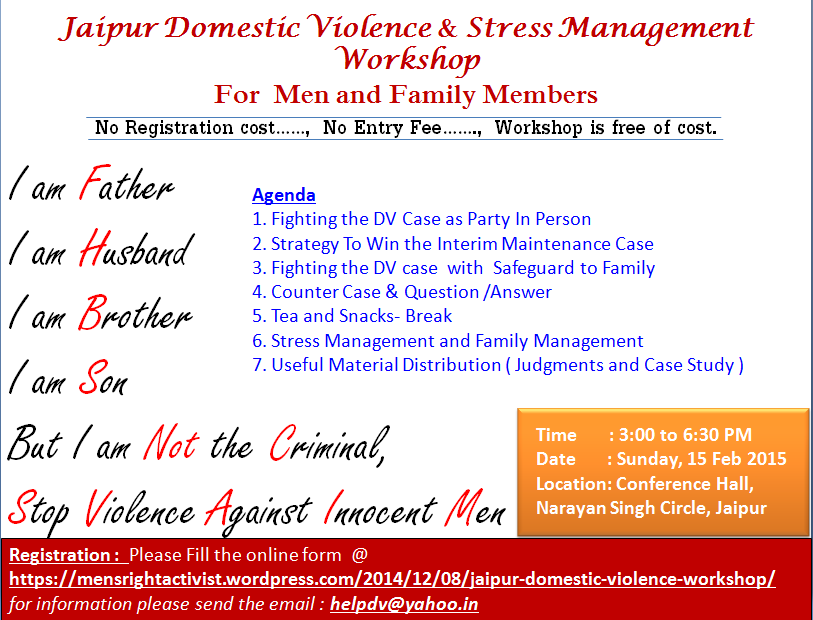

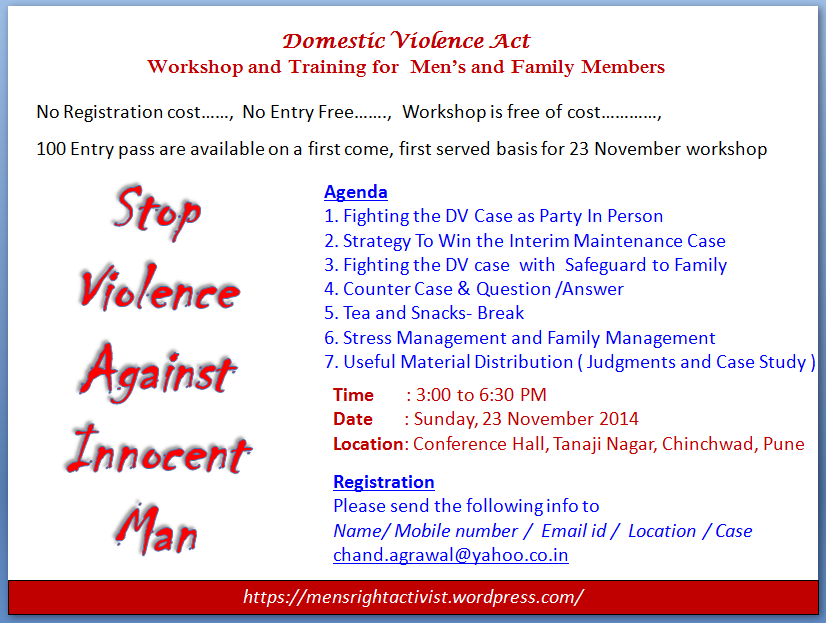

1. 15 Feb 2015 : Free Domestic Violence Workshop in Jaipur

2. 22 Feb 2015 : Free Domestic Violence Workshop in Mumbai

Check Important Link

Stop Violence Against Innocent Man

Domestic violence workshop

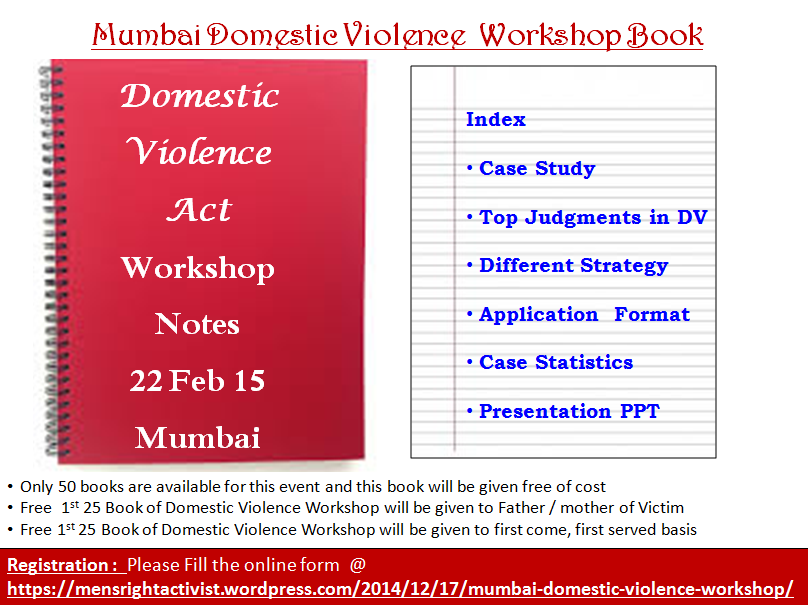

Only 400 Seat and 50 Book are available for this event

Entry pass are available on a first come, first served basis for 22 Feb workshop

Only 50 books we are printing for this event and this book will be given to free of cost

Free 1st 25 Book of Domestic Violence Workshop will be given to All the Senior Citizen or Father / mother of Victim

Check Important Link

Please provide the below information and Click submit for the Registration

Stop Violence Against Innocent Man

Domestic violence workshop

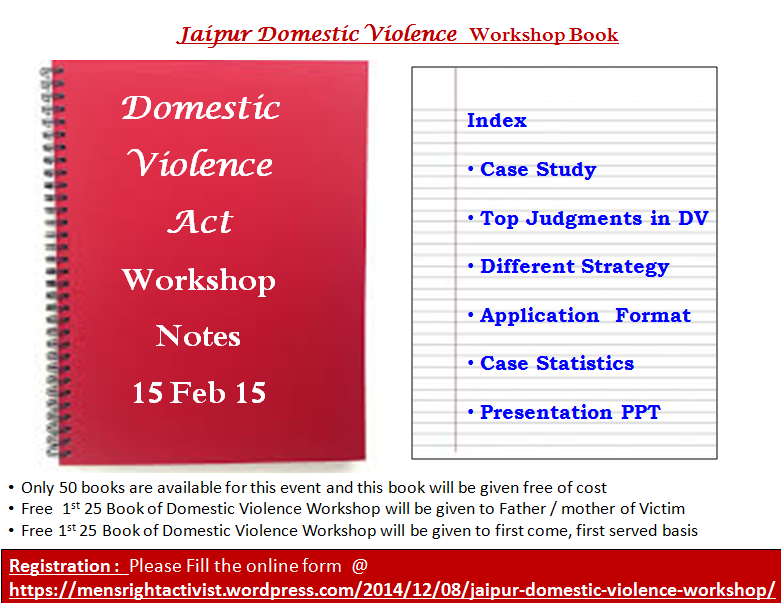

Only 300 Seat and 50 Book are available for this event

Entry pass are available on a first come, first served basis for 15 Feb workshop

Only 50 books we are printing for this event and this book will be given to free of cost

Free 1st 25 Book of Domestic Violence Workshop will be given to All the Senior Citizen or Father / mother of Victim

Check Important Link

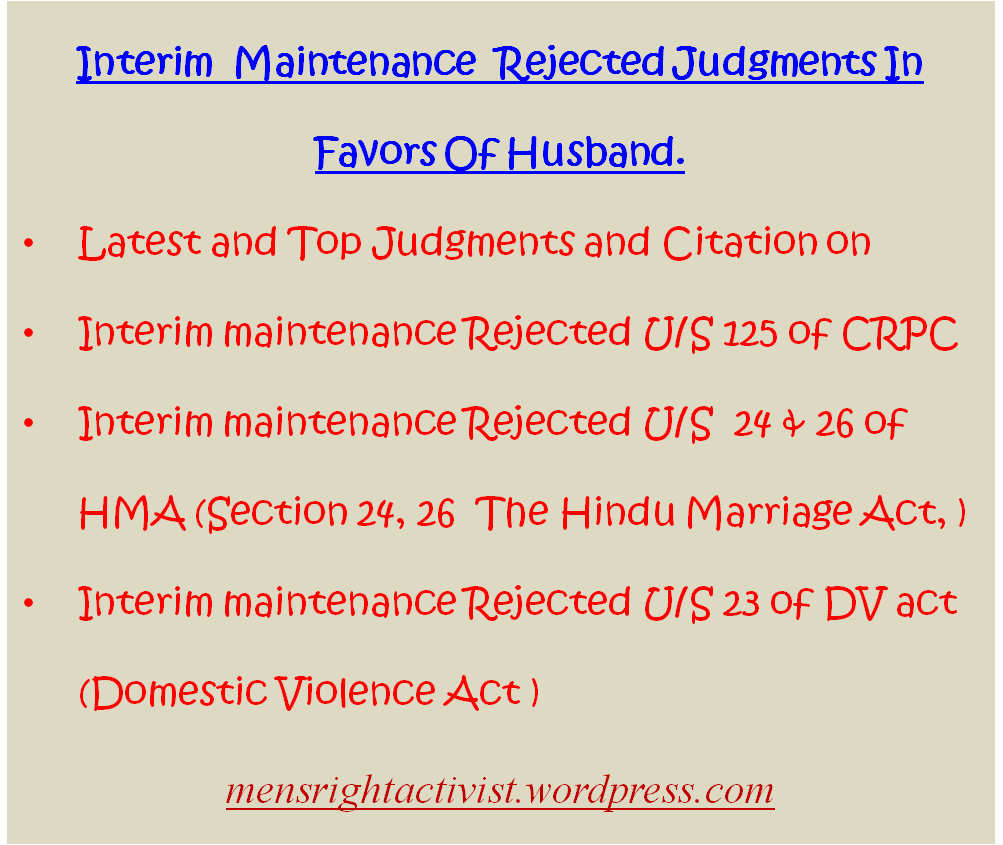

Interim maintenance Rejected Judgments in favor of husband.

Latest and Top Judgments and Citation on

Interim maintenance Rejected U/S 24 & 26 of HMA

(Section 24, 26 The Hindu Marriage Act, )

No Interim/Maintainance for Capable,Working Women

IN THE HIGH COURT OF MADHYA PRADESH (INDORE BENCH) Civil Revision No. 1290/99 Decided On: 24.03.2000, Appellants: Smt. Mamta Jaiswal Vs. Respondent: Rajesh Jaiswal, Hon’ble Judges:J.G. Chitre, J. Acts/Rules/Orders:Hindu Marriage Act, 1955 – Sections 24 and 26

6. In view of this, the question arises as to in what way Section 24 of the Act has to be interpreted. Whether a spouse who has capacity of earning but chooses to remain idle, should be permitted to saddle other spouse with his or her expenditure ? Whether such spouse should be permitted to get pendente life alimony at higher rate from other spouse in such condition ?

According to me, Section 24 has been enacted for the purpose of providing a monetary assistance to such spouse who is incapable of supporting himself or herself in spite of sincere efforts made by him or herself. A spouse who is well qualified to get the service immediately with less efforts is not expected to remain idle to squeeze out, to milk out the other spouse by relieving him of his or her own purse by a cut in the nature of pendente life alimony. The law does not expect the increasing number of such idle persons who by remaining in the arena of legal battles, try to squeeze out the

adversory by implementing the provisions of law suitable to their purpose. In the present case Mamta Jaiswal is a well qualified woman possessing qualification like M. Sc. M.C. M.Ed. Till 1994 she was serving in Gulamnabi Azad Education College. It impliedly means that she was possessing sufficient experience. How such a lady can remain without service ? It really puts a big question which is to be answered by Mamta Jaiswal with sufficient congent and believable evidence by proving that in spite of sufficient efforts made by her, she was not able to get service and, therefore, she is unable to support herself. A lady who is fighting matrimonial petition filed for divorce, can not be permitted to sit idle and to put her burden on the husband for demanding pendente lite alimony from him during pendency of such matrimonial petition. Section 24 is not meant for creating an army of such idle persons who would be sitting idle waiting for a ‘dole’ to be awarded by her husband who has got a grievance against her and who has gone to the Court for seeking a relief against her. The case may be vice-versa also. If a husband well qualified, sufficient enough to earn, sits idle and puts his burden on the wife and waits for a ‘dole’ to be awarded by remaining entangled in litigation. That is also not permissible. The law does not help indolents as well idles so also does not want an army of self made lazy idles. Everyone has to earn for the purpose of maintenance of himself or herself, atleast, has to make sincere efforts in that direction. If this criteria is not applied, if this attitude is not adopted, there would be a tendency growing amongst such litigants to prolong such litigation and to milk out the adversory who happens to be a spouse, once dear but far away after an emerging of litigation. If such army is permitted to remain in existence, there would be no sincere efforts of amicable settlements because the lazy spouse would be very happy to fight and frustrate the efforts of amicable settlement because he would be reaping the money in the nature of pendente lite alimony, and would prefer to be happy in remaining idle and not bothering himself or herself for any activity to support and maintain himself or herself. That can not he treated to he aim, goal of Section 24.

It is indirectly against healthyness of the society. It has enacted for needy persons who in spite of sincere efforts and sufficient efforts arc unable to support and maintain themselves and arc required to fight out the litigation jeopardising their hard earned income by toiling working hours.

8. In fact, well qualified spouses desirous of remaining idle, not making efforts for the purpose of finding out a source of livelihood, have to be discouraged, if the society wants to progress. The spouses who are quarrelling and coming to the Court in respect of matrimonial disputes

No interim maintenance to earning wife having sufficient means.

Madras High Court, Hindu Marriage Act , Manokaran alias Ramamoorthy vs M Devaki, Citation: (2003) I MLJ 752 (Mad) ,Judgment date 21 Feb 2003

Link : http://indiankanoon.org/doc/54216/

No maintenance to earning spouse”, “Interim maintenance not for parity between spouses

Delhi High Court, Hindu Marriage Act, Manish Kumar vs Pratibha, Judgment dated 18 Sep 2008

Educated employable wife not entitled to maintenance

Madhya Pradesh High Court, Hindu Marriage Act, Mamta Jaiswal vs Rajesh Jaiswal, Equivalent Citation: 2000 (4) MPHT 457 ,Judgment date: 24 March 2000

Link : http://indiankanoon.org/doc/1728023/

Petitioner being employed and living separate and being a major having her own independent source of income was not entitled to relief.

IN THE HIGH COURT OF DELHI AT NEW DELHI + CRL.MC No. 3325/2010, KAVERI ….. Petitioner versus Neel Sagar & Anr. ….. Respondents CORAM: JUSTICE SHIV NARAYAN DHINGRA

Linke http://indiankanoon.org/doc/141414000/

Interim maintenance Rejected U/S 125 of CRPC

INTERIM REJECTED AS WIFE IS ABLE TO SUSTAIN: If wife is able to sustain herself no interim maintenance court observed as follows: – Chaturbhuj Vs Sita Bai in CASE NO 1627 of 2007.

Court: IN THE SUPREME COURT OF INDIA, Bench: Dr. ARIJIT PASAYAT & AFTAB ALAM, CRIMINAL APPEAL No: 1627 of 2007, DATE OF JUDGMENT: 27/11/2007

In the application it was claimed that she was unemployed and unable to maintain herself…..

…..The phrase “unable to maintain herself” in the instant case would mean that means available to the deserted wife while she was living with her husband and would not take within itself the efforts made by the wife after desertion to survive somehow…..

6. Under the law the burden is placed in the first place upon the wife to show that the means of her husband are sufficient. In the instant case there is no dispute that the appellant has the requisite means.

7. But there is an inseparable condition which has also to be satisfied that the wife was unable to maintain herself. These two conditions are in addition to the requirement that the husband must have neglected or refused to maintain his wife. It is has to be established that the wife was unable to maintain herself.The appellant has placed material to show that the respondent-wife was earning some income. That is not sufficient to rule out application of Section 125 Cr.P.C. It has to be established that with the amount she earned the respondent-wife was able to maintain herself.

8. In an illustrative case where wife was surviving by begging, would not amount to her ability to maintain herself. It can also be not said that the wife has been capable of earning but she was not making an effort to earn.

Link :http://indiankanoon.org/doc/1720873/ http://judis.nic.in/supremecourt/imgs1.aspx?filename=29928

No Interim maintenance for Wife if she lives separate from Husband without sufficient cause:

Court: HIGH COURT OF JUDICATURE AT MADRAS, Bench: MR.JUSTICE P.R.SHIVAKUMAR, CRIMINAL APPEAL No: Crl.R.C.No.1491 OF 2005, DATE OF JUDGMENT: 22.2.2008

Marimuthu vs Janaki for Crl.R.C.No.1491 OF 2005 court observed as follows:

“Sub Clause 4 of Section 125 Cr.P.C., contended that a wife who is living away from her husband by mutual consent between the husband and wife, would not be entitled to an order of maintenance under Section 125 Cr.P.C. sub Sections 4 and 5 of 125 Cr.P.C. are reproduced as hereunder:-

"(4) No wife shall be entitled to receive an allowance for the maintenance or the interim maintenance and expenses of proceeding, as the case may be, from her husband under this section if she is living in adultery, or if, without any sufficient reason, she refuses to live with her husband, or if they are living separately by mutual consent.”

Link : http://indiankanoon.org/doc/895661/ http://judis.nic.in/judis_chennai/qrydisp.aspx?filename=13342

No interim maintenance to previously working wife

Court: HIGH COURT OF DELHI AT NEW DELHI, Bench: SHIV NARAYAN DHINGRA,CM(M) No: 1790/2006 and CM No. 14635/2006 18.09.2008 ,DATE OF JUDGMENT:September 18 2008

The maintenance is to be fixed on the basis of actual earnings of a person and not on his being able bodied person. In this country, there is no job guarantee given by the government to every able bodied person. Many able bodied persons are jobless in our country. The only job guarantee is under National Rural Employment Guarantee Scheme under which 100 days labour work is assured to an unemployed rural person. The husband does not qualify for that. Moreover, the wife is equally able bodied. The wife has failed to show, in this case, any earning of the husband. She did not dispute the facts stated that the van was sold by her, the house was sold by her and she was facing a case filed by the father of the husband in respect of illegal sale of the house. The amount received from sale of the house is with the wife and she must be earning interest on it. She has failed to show any source of income to the husband. The bald allegation of his doing tuition without stating as to what was his educational qualification and to whom he was teaching, would not serve the purpose.

8. I find that the order of the learned ADJ was based on no material and was simply made on the ground that the husband was an able bodied person. The order of maintenance is not tenable and is hereby set aside. However, the husband is liable to pay the litigation expenses as fixed by the trial Court

Link: https://groups.yahoo.com/neo/groups/DVhelp/info

“Maintenance rejected as the Woman is well qualified, employed earlier and quitted the job on her own will.”

Court: IN THE HIGH COURT OF DELHI AT NEW DELHI, Author: HON’BLE MS. JUSTICE PRATIBHA RANI, Crl. Rev. P. No: CRL.REV.P. 344/2011, Date:19.04.2012

Interim maintenance Rejected U/S 23 of DV act (Domestic Violence Act )

“REFUSE MAINTENANCE TO WOMEN IN DV CASE.”

Court: HIGH COURT OF DELHI AT NEW DELHI ,Author: HON’BLE MR. JUSTICE SURESH KAIT, Crl. Rev. P. No: CRL.M.C. No.2602/2010 , Date:30th January, 2012

Before awarding maintenance, the Courts are required to take note of the income of the husband and also the probable income of the wife. R.Ramu Vs. Smt. Leelavathi, HON’BLE JUSTICE Ajit J. Gunjal, J. Date of Judgment : 07/12/2009 Writ Petition No. 2118 of 2009 2010 (1) KarLJ 376 .

In order to substantiate above averments and in order to enlighten upon the subject, I am bringing kind attention of Hon’ble court about the ratio decided laid down by different higher courts of our country. One such point is the care that should be adopted by Magistrate court in disposing interim application regarding Domestic violence case. PARTIES: Razia Begum vs State Nct Of Delhi & Ors, Crl.MC- 4246/09 & 4375/09, COURT: DELHI HIGH COURT, Date of Order: 4th October, 2010, BENCH: JUSTICE SHIV NARAYAN DHINGRA, AVAILABLE SOURCE:- http://indiankanoon.org/doc/1404656/ , http://lobis.nic.in/dhc/ :– It has to be noticed that although Domestic Violence Act is not a penal law but it is a peculiar Act where non-compliance of the order passed under the Act has been made as an offence under Section 31 of the Act and an FIR can be registered against the person who does not comply with the order and this offence is triable by the same Magistrate who passed the interim order for protection or maintenance. In view of this provision under Section 31, it becomes incumbent and responsibility of the Magistrate to be careful in passing order and to specify as to whether there was domestic relationship between the aggrieved person and the respondent and who was the person responsible for compliance of the order.

Wife is living separately without any appropriate reasons:

Court: HIGH COURT OF UTTARAKHAND, Bench: Alok Singh, J. CRIMINAL APPEAL No: 201 Of 2006, DATE OF JUDGMENT:November 18, 2009

In smt. Archana Gupta vs Sri Rajeev Gupta for Criminal Revision No. 201 Of 2006, court observed as follows: I, myself, carefully perused the statements recorded by learned trial court. I find no perversity in the findings of fact recorded by learned Principal Judge, Family Court, Dehradun of the fact that wife is living separately without any sufficient cause and reason and she refused to live with her husband without any sufficient reason. In view of findings that wife is residing separately from her husband without reasonable cause and reason, her application seeking maintenance was rightly rejected by the learned trial Court.

Link :http://indiankanoon.org/doc/1746587/

No Maintenance if wife wants to reside separately:

Bombay High Court Mrs. Meena Dinesh Parmar vs Shri Dinesh Hastimal Parmar on 4 February, 2005 Bench: H Gokhale, R Mohite JUDGMENT R.S. Mohite, “

…We find from the evidence of the husband that the main reason given by him as to why his wife was unhappy was that she was seeking a separate accommodation and desired to stay away from the joint family. He has stated that his wife denied physical relations with him and caused him physical and mental torture …

… We find no justification in the contention of the wife for staying at Pune with her maternal uncle, even though her husband had purchased a separate place for their exclusive residence. Such an act on her part of staying at Pune along with her newly born son does amount to both cruelty as well as desertion and no fault can be found in the impugned judgment and order granting divorce on the ground of cruelty and desertion.

6. So far as question of maintenance is concerned, in view of our aforesaid finding, maintenance cannot be granted to the wife.

Link:http://indiankanoon.org/doc/1401220/

No Maintenance If Wife Lies

Court: IN THE SUPREME COURT OF INDIA Bench: G.S. Singhvi and Asok Kumar Ganguly, JJ, Civil Appeal No. 5239 of 2002 ,DATE OF JUDGMENT: 03.12.2009

Check Important Link

Counter case in 498a and DV

Counter Case Logic after false 498a, DV and CrPC 125

If your dear and lovely wife filed the flase 498a, DV act, Crpc 125 then 1st question you will ask to your Lawyer and friend like which counter case I can filed on my wife for Revenge

“ Revenge is often like biting a dog because the dog bit you”

In Indian Law system we can divide the counter case into Four Category

Why should we filed the Counter case in Family dispute ?

If you use counter case as just another strategy in your game plan to exit from your family dispute and put the wife in back sit it worked like Wonder…!

But well well ….. !

If you use counter case to harassed your wife and take the revenge then most of the time it backfire. End result you will end up with nothing..! 🙂

Counter case can be divided into 3 pursues

“What is of supreme importance in war is to attack the enemy’s strategy not the enemy”

When to filed the count case

When you are planning to attack make sure following important points

1. Secure your self and your family member as 1st priority ( like bail, acquittal, Quash etc )

2. Make sure you sufficient Time / Energy / Resource / Money to fight the cases

3. Make sure that 80% safety 1st and 20% attacked strategy

4. Best time to file the counter case is after the CROSS of wife or after the case is over as per strategy

5. Let’s 1st give the chance to wife and let her expose all her evidence.

6. Understand the opposite party strategy by giving her proper time to let her utilized all her resource / energy / contacts etc

7. Make sure your attack will hit 101%,

Introspection to Check before filing the counter case

1. It will increase the litigation

2. Your resource utilization like time / energy / money / effort and Lawyer follow-up

3. Each counter case has it own time limit ( for example Defamation case need to file in specific time frame or DP act has one year time limit )

4. Delayed justices system in India

5. Corrupt System and Favoritism towards women.

6. It will disputed your life peace and future plan.

7. Some time it may backfire

8. Each counter case and section has it’s own merit, advantage and dis-advantage

Defamation cases are of 2 types:

1. Civil defamation where you will claim monetary compensation.

2. Criminal defamation where you will seek punishment to the offenders.

Don’t think these cases will win ultimately and anyone will fight it till end BUT these weapons can scare the opposite side and her supporters and eventually force them to come for a Divorce and withdrawal of all cases against you.

TEP ( Tax Evasion Petition) : This is extrajudicial weapons this do not increase your ligitation but it will be very helpfull to dissmiss the DV and 498a and also put the pressure on opposite party do not dealy the filing TEP in your case if you have proper merit of TEP in your case filied ASAP at the Income Tax Commissioner and also at the Commercial Taxes Commissioner (state)

Check the TEP format

If FIL or MIL are govt employees, approach their offices if they have said anywhere of giving dowry. Use RTI to get information. You can also file DP3 against the in-laws if they said anywhere on oath that dowry was given.

Some are the important IPC section used in False case are

CRPC 340 AN EFFECTIVE TOOL TO COUNTER AND TO DEFEND

• 191. Giving false evidence

• 192. Fabricating false evidence

• 193 Punishment for False evidence

• 195. Giving or fabricating false evidence with intent to procure conviction of offence punishable with imprisonment for life or imprisonment.

• 199. False statement made in declaration which is by law receivable as evidence.

• 200. Using as true such declaration knowing it to be false

• 209. Dishonestly making false claim in Court

• 211. False charge of offence made with intent to injure

Defamation.

• 499. Defamation.

• 500. Punishment for defamation.

Extortion ( IPC.Section:383 to 389 )

• PC Sec: 384 (Punishment for extortion): Whoever commits extortion shall be punished with imprisonment of either description for a term which may extend to three years, or with fine, or with both.

• IPC Sec: 385 (Putting person in fear of injury in order to commit extortion)

• IPC Sec: 386 (Extortion by putting a person in fear of death or grievous hurt to)

• IPC Sec: 387 (Putting person in fear of death or of grievous hurt, in order to commit extortion)

• IPC Sec: 388 (Extortion by threat of accusation of an offence punishable with death or imprisonment for life, etc)

• IPC Sec: 389 (Putting person in fear of accusation of offence in order to commit extortion)

If you want to attack first, document her greedy demands in some form (email, phone recording, letter, third party witnesses, etc) and then file a criminal case in India under IPC 389.

Definition of IPC 389:Indian Penal Code IPC-389

Putting person in fear of accusation of offence, in order to commit extortion.

Classification : According to Para 1 – This section is Non-bailable, Cognizable and Non-compoundable.

Triable By : Magistrate of the first class.

Punishment : According to Para 1 – Imprisonment for 10 years and fine.

Depend upon your strategy you can use the following Section for Counter case

After the case is over you can follow the following step

1. Press Release to with detail and let society know the false and frivolous cases are reality

2. Filied the 499/ 500 or 182 or any such other cases

Wait for more blog with detail of each counter case and advantage and disadvantage

Check Important Link

TEP and RTI Tax Evasion Petition Judgment, Citation

Useful Judgment while filing the TEP

In-Laws should disclose source of income for the exorbitant claims in 498a and DV case

Regarding False dowry allegations, Interpretation of the statute by delhi High Court. PARTIES: SMT NEERA SINGH VS STATE OF DELHI, DELHI HC, COURT: DELHI HIGH COURT, Date of Order: on 23 February, 2007, BENCH: JUSTICE SHIV NARAYAN DHINGRA, AVAILABLE SOURCE:- http://indiankanoon.org/doc/1061764/ , http://lobis.nic.in/dhc/ :- Had given a landmark judgment that deals with the issue of Dowry allegations: “Now-a-days, exorbitant claims are made about the amount spent on marriage and other ceremonies and on dowry and gifts. In some cases claim is made of spending crores of rupees on dowry without disclosing the source of income and how funds flowed. I consider time has come that courts should insist upon disclosing source of such funds and verification of income from tax returns and police should insist upon the compliance of the Rules under Dowry Prohibition Act and should not entertain any complaint, if the rules have not been complied with. If huge cash amounts are alleged to be given at the time of marriage which are not accounted anywhere, such cash transactions should be brought to the notice of the Income Tax Department by the Court so that source of income is verified and the person is brought to law. It is only because the Courts are not insisting upon compliance with the relevant provisions of law while entertaining such complaints and action is taken merely on the statement of the complainant, without any verification that a large number of false complaints are pouring in.” ………… The Metropolitan Magistrates should take cognizance of the offence under the Act in respect of the offence of giving dowry whenever allegations are made that dowry was given as a consideration of marriage, after demand. Courts should also insist upon compliance with the rules framed under the Act and if rules are not complied with, an adverse inference should be drawn. If huge cash amounts are alleged to be given at the time of marriage which are not accounted anywhere, such cash transactions should be brought to the notice of the Income Tax Department by the Court so that source of income is verified and the person is brought to law. It is only because the Courts are not insisting upon compliance with the relevant provisions of law while entertaining such complaints and action is taken merely on the statement of the complainant, without any verification that a large number of false complaints are pouring in. ………. I consider that the kinds of vague allegations as made in the complaint by the petitioner against every member of the family of husband cannot be accepted by any court at their face value and the allegations have to be scrutinized carefully by the Court before framing charge. A perusal of the complaint of the petitioner would show that she made all kinds of false allegations against her husband regarding beating, forced to buy the CAR, abused her, taunted her, threatened. However, in her complaint, she made vague and omnibus allegations against every other family members.

Useful judgment whiling filing the TEP+RTI

TEP investigation and outcome must be provided to appellant

CIC:: File No.CIC/RM/A/2013/000635, Appellant: Shri Om Prakash Singh, New Delhi

DECISION:: It has been the consistent stand of the Commission that some sort of a feedback should be provided to the information provider once investigation into a tax evasion complaint has been finalized. The complainant has a right to know whether the information provided by him has been found to be false or true. We accordingly direct the CPIO to disclose the broad outcome of the TEP to the appellant once the enquiry is completed. Details of investigation are, however, not required to be disclosed.

http://www.rti.india.gov.in/cic_decisions/CIC_RM_A_2013_000635_M_121813.pdf

CPIO to disclose the broad outcome of the TEP to the appellant in 04 months time

CIC:: File No. CIC/LS/A/2009/001067 Appellant – Shri Manish Kumar, Date of Decision 04.03.2010

DECISION:: In view of the above discussion, the CPIO is hereby directed to disclose the broad outcome of the TEP to the appellant in 04 months time. It is, however, clarified that he need not disclose the details of investigation.

Judgment is available on dvhelp@yahoogroup.com

TEP investigation and outcome must be provided to the appellant in 03 months time and CPIO must provide the information under CrPC 91

CIC:: File No.CIC/LS/A/2009/001113 Appellant : Shri Chetan Anand Parashar, Date of Decision : 19.2.2010

DECISION :: 7. In view of the above discussion, the decisions of CPIO and AA in regard to non-disclosure of ITRs are upheld. Even so, the CPIO is directed to intimate the outcome of TEP to the appellant in 03 months time.

8. Before parting with the matter, we would like to mention that section 91 of Code of Criminal Procedure empowers a court or an officer in charge of a Police Station to seek production of any documents for the purpose of investigation, inquiry or trial etc, pending before such court or officer. It is open to the appellant to take resort to this provision, if he is so advised.

Judgment is available on dvhelp@yahoogroup.com

TEP investigation should not and infinitum and that it should be concluded in a reasonable time frame

CIC:: File No. CIC/LS/A/2009/001179 ( Appellant – Sh. Virag R. Dhulia ) /Date of decision – 18.02.2010

5. It is to be noted that investigation into a TEP cannot be allowed to go on ad-infinitum and that it should be concluded in a reasonable time frame whereafter the broad outcome thereof needs to be communicated to the appellant i.e. whether the allegations made in the TEP are fully true, partially true or untrue. No further information needs to be disclosed at this stage.

DECISION :: 6. In view of the above, Income Tax Officer, Ward 31(3), 10 – B.C., Middleton Row, Kolkata-700017, is hereby directed to complete the investigation in next three months time and intimate the broad outcome thereof, as indicated herein above, to the appellant in three months time.

Judgment is available on dvhelp@yahoogroup.com

Income tax department should provide the Father in Law Income tax detail

CIC :: Appeal : No. CIC/LS/A/2010/001044DS Appellant /Complainant : Sh. Manoj Kumar Saini, Jaipur Date of Decision : 24 March, 2011

18. We direct the CPIO to furnish the information pertaining to the net taxable income of Shri Munna Lal Saini, the fatherinlaw of the Appellant, for the period of year 2000 till 15.09.2009 (i.e. the date of the Appellant’s RTI Application) to the Appellant within 10 days.

Judgment is available on dvhelp@yahoogroup.com

TEP should finish within 3 months,

CIC :: File No.CIC/LS/A/2009/001113 Appellant : Shri Chetan Anand Parashar Date of Decision : 19.2.2010

held as follows :-

7.In view of the above discussion, the decisions of CPIO and AA in regard to non disclosure of ITRs are upheld. Even so, the CPIO is directed to intimate the outcome of TEP to the appellant in 03 months time.

In another decision dated 18.02.2010 in Virag R Dhulia Vs IT Department, Kolkatta File No.CIC/LS/A/2009/001179, the single Bench headed by the undersigned had held as follows :

“……………(6)In view of the above, Income Tax Office, Ward No.31(3), 20, BC Middleton Row, Kolkatta – 700017 is hereby directed to complete the investigation in next three months time and intimate the broad outcome thereof, as indicated herein above, to the appellant in three months time.

Judgment is available on dvhelp@yahoogroup.com

Similar judgement

1. Judgment from CENTRAL INFORMATION COMMISSION in CIC/AT/A/2008/0268. Where Information Commissioner allows the similar petition TEP information allowed and cannot be said to be a personal matter of the tax evader not exempted under Sec 8(1) of the RTI Act.

2.Judgment from CENTRAL INFORMATION COMMISSION in Wide Decision No.174/IC (A)/2006. Where Information Commissioner allows the similar petition TEP information and its outcomes should be disclosed not exempted under Sec 8(1) of the RTI Act.

3.Judgment from CENTRAL INFORMATION COMMISSION inCIC/AT/A/2008/01389. Where Information Commissioner allows the similar petition RTI of dowry matter allowed and hereby directed to disclose the above mentioned not exempted under Sec 8(1) of the RTI Act.

4.Judgment from CENTRAL INFORMATION COMMISSION inCIC/SG/C/2009/000702/4128. Where Information Commissioner where he defines the concept of privacy, fundamental right of the Complainant as provided under Article 21 of the Constitution.

5.Judgment from CENTRAL INFORMATION COMMISSION inCIC/WB/A/2007/00064. Where Information Commissioner explains about the “sensitive personal data” means personal data consisting of information.

6.Judgment from CENTRAL INFORMATION COMMISSION inCIC/LS/A/2010/001044DS. Where Information Commissioner allows the similar petition TEP information allowed related to dowry and not exempted under Sec 8(1) of the RTI Act.

7.Judgment from CENTRAL INFORMATION COMMISSION inCIC/DS/A/2011/002918/RM. Where Information Commissioner allows the similar petition TEP information allowed related to dowry and not exempted under Sec 8(1) of the RTI Act.

8.Judgment from CENTRAL INFORMATION COMMISSION inCIC/DS/A/2011/003358. Where Information Commissioner allows the similar petition of the IT Return allow in dowry case is not exempted under Sec 8(1) of the RTI Act.

9.Judgment from CENTRAL INFORMATION COMMISSION inCIC/DS/A/2011/003359. Where Information Commissioner allows the similar petition TEP information allowed and not exempted under Sec 8(1) of the RTI Act.

UusefulJudgement

10 If CPIO disclose TEP info then doubt of black money will be removed from husband mind and this way the information will fulfill the objective of RTI to check the corruption as said by Hon’ble justice Shri Pradeep Kant (Allahabad High Court) in the recent judgment under Writ Petition No. 3262 (MB) of 2008, Public Information Officer Vs. State Information Commission, U.P. and others,

“….Our Constitution establishes a democratic republic. Democracy requires an informed citizenry and transparency of information which are vital to its functioning……..The purpose and object of the act is not only to provide information but to keep a check on corruption, and for that matter confers a right upon the citizens to have the necessary information,

11 .Honorable Central Information Commissioner Prof. M.M. Ansari Wide Decision F. No.CIC/MA/A/2006/00108.

The appellant has mentioned the reason, as above, for seeking information on the Tax Evasion Petition (TEP) filed by him against his wife. The aspects of strained human relations that may become the reason for seeking information is out of the purview of our mandate. However, the public actions, irrespective of the cause of such actions, and disclosure of its outcome, fall under the domain of RTI Act. The action taken on TEP has to be examined accordingly.

On the issue of progress report on TEP, it has been observed that:

“Investigations of the complaint on tax evasion by the IT department is a part of the process of identifying the offenders and assessing the extent of tax evasion by them. Until the nature of offence is duly examined and thoroughly investigated and necessary action is taken under the relevant provisions of tax laws, the disclosure of investigation report on tax evasion is barred u/s 8(1) (h).

Needless to say, the Department of Income Tax is expected to conduct investigations fairly and objectively, and that in a transparent manner, so that the relevant investigation report could be made public, soon after the taxes due from the offenders are recovered”. (Ref. Appeal No.34/IC(A)/06 dated 4th May 2006)

As the investigations on TEP have been conducted by DIT (Inv.), the relevant report is the outcome of public action, which needs to be disclosed. This, therefore, cannot be exempted u/s 8(1)(j) as interpreted by the appellate authority.

Accordingly, DIT (Investigation) is directed to disclose the report as per the provision u/s 10 (1) & (2), after the entire process of investigation and tax recovery,

if any, is complete in every respect.

12.Honorable Chief Information Commissioner Shri Shailesh Gandhi Wide Decision No. CIC/LS/A/2009/000647/SG/5887 dated 14-12-2009 in TEP / RTI matter where he defines the concept Section 8(1)(h) of the Act provides-

8. (1) Notwithstanding anything contained in this Act, there shall be no obligation to give any citizen,—

(h) information which would impede the process of investigation or apprehension or prosecution of offenders;

Dr. Naresh Trehan, one of the third parties, and the Department have relied on this ground of exemption. Both parties have stated that as the process of assessment has not been finalized till date and Investigation is still underway, exemption under Section 8(1)(h) applies. But the mere fact that an investigation is underway and that assessment has not been finalized is not a sufficient ground for the application of Section 8(1)(h).

13 The High Court of Delhi has held in Bhagat Singh v. CIC & Ors. WP (C) No. 3114/2007 that-

“It is apparent that the mere existence of an investigation process cannot be a ground for refusal of the information; the authority withholding information must show satisfactory reasons as to why the release of such information would hamper the investigation process. Such reasons should be germane, and the opinion of the process being hampered should be reasonable and based on some material. Sans this consideration, Section 8(1)(h) and other such provisions would become the haven for dodging demands for information” The PIO has contention that,

“Logically no investigation could be said to be complete unless it has reached a point where the final decision on the basis of that investigation is taken. In this context the progress of assessments are therefore exempt from disclosure under Section 8(1)(h)”, only states that the investigation is not over. No claim has been made that the process of investigation would be impeded in any manner.

Neither party has been able to establish before the Commission how the disclosure of information to the Appellant would impede the process of investigation. Therefore, Section 8(1)(h) cannot be applied in the present case to claim exemption from disclosure of information.

The disclosure of the information would lead to unwarranted invasion of the privacy of the individual.

Certain human rights such as liberty, freedom of expression or right to life are universal and therefore would apply uniformly to all human-beings worldwide. However, the concept of ‘privacy’ is a cultural notion, related to social norms, and different societies would look at these differently. Therefore referring to laws of other countries to define ‘privacy’ cannot be considered a valid exercise to constrain the Citizen’s fundamental Right to Information in India. Parliament has not codified the right to privacy so far, hence in balancing the Right to Information of Citizens and the individual’s Right to Privacy the Citizen’s Right to Information would be given greater weightage.

14. Honorable Central Information Commissioner Prof. M.M. Ansari Wide Decision No.174/IC(A)/2006 in same kind of TEP/RTI matter :

Every action taken by public bodies or public servants and its outcome should be under the domain of public for open scrutiny. It follows that the proceedings initiated by the income-tax department, in pursuance of the tax evasions petition (TEP), and its outcomes should be disclosed, even without asking for such information by the petitioners.

As regards the disclosure of tax assessment orders passed by the assessing officers is concerned, such documents should also be disclosed provided that larger public interest such as containing corruption is served. In the present case, the appellant has not established as to what is the overriding public interest in disclosing the details of tax assessment orders which contains confidential business and financial transactions of the assessees. Unless the case of public interest is established, the disclosure of such information would tantamount to unwarranted invasion of privacy of assessees. Therefore, the decision of appellate authority is upheld. The CPIO is, however, directed to furnish the Action Taken Report on the TEP filed by the appellant. The appeal is accordingly disposed of.

15. Honorable Information Commissioner Shri Sailesh Gandhi of CIC bearing his Decision No. CIC/SG/C/2009/000702/4128 dated 14-07-2009 where he defines the concept of privacy ,which may act as a guidance for every public information officer

This information is very important for the Complainant as he is facing a threat of arrest and needs the information to prove his innocence. Not granting such information clearly leads to violation of the fundamental right of the Complainant as provided under Article 21 of the Constitution. If The Complainant has more than one way of seeking remedy he has the freedom to opt for the way which is more convenient for him. No claim has been made by the PIO of any exemption under the RTI Act to deny the information. If a Public Authority has a procedure of disclosing certain information which can also be accessed by a Citizen using the Right to Information Act, it is the Citizen’s prerogative to decide which route he wishes to take. The existence of another method of accessing information cannot be a justification to deny the Citizen his freedom to exercise his fundamental right codified under the Right to Information Act. If the Parliament wanted to restrict this right, it would have been stated expressly in the Act. Nobody else has the right to constrain or limit the rights of the Sovereign Citizen. There is no provision in the Right to Information Act which restrains the Citizen’s right to use it if another route to access information has been offered. It is a Citizen’s right to use the most convenient and efficacious means available to him.

16. “In Peoples Union of Civil Liberties Vs. Union of India, however, in his judgment of 13.2.2003 Shri P.V. Reddy J. has ruled as follows :

“When there is a competition between the right to privacy of an individual and the right to information of the citizens, the former right has to be subordinated to the latter right as it serves larger public interest. The right to know about the candidate who intends to become a public figure and a representative of the people would not be effective and real if only truncated information of the assets and liabilities is given.”

17 That False Dowry cases are a matter of “larger public interest” and that the information relating to IT returns of in-laws be furnished to husband,

From the paragraph 14 of the attached CIC judgment (Appeal : No. CIC/LS/A/2010/001044DS)

14. The mandate of the RTI Act to disclose personal information under Section 8(1)(j) is even stricter since it appends the expression “larger” to “public interest”. Mere public interest will not suffice in the disclosure of personal information such as the IT Returns of an assessee unless the Applicant can prove that a “larger” public interest demands such disclosure. The expression “larger” cannot be defined or carved into a straight jacketed formula and neither can it be easily disposed of. If the Applicant incessantly stresses on the argument that false dowry cases are a matter of “larger public interest” and that the information relating to IT returns of his father in law be furnished to him, then an equally challenging rebuttal could be that the Income Tax Act, which defines the procedure of disclosure of such IT Returns to him, is a public policy which has been enacted by the State keeping in mind the larger good of the society. It is not the case of the Respondents that objection to disclosure of the documents is taken on the ground that it belongs to a class of documents which are protected irrespective of their contents, because there is no absolute immunity for documents belonging to such class.

18. That, husband fighting criminal cases against “State of Maharashtra”. The “State” is pursuing a criminal case against husband and that since “State” has decided to prosecute me because of legal fiction created under Section 405 of IPC, automatically a “larger public interest” is involved in the matter.

From the paragraph 13 of the attached CIC judgment (Appeal : No. CIC/LS/A/2010/001044DS)

13. It brings me to the second contention of the Appellant which revolves around the concept of “larger public interest”. According to the Appellant, the “State” is pursuing a criminal case against him and that since “State” has decided to prosecute him because of legal fiction created under Section 405 of IPC, automatically a “larger public interest” is involved in the matter. Section 405 of the IPC states that “Whoever, being in any manner entrusted with property, or with any dominion over property, dishonestly misappropriates or converts to his own use that property, or dishonestly uses or disposes of that property in violation of any direction of law prescribing the mode in which such trust is to be discharged, or of any legal contract, express or implied, which he has made touching the discharge of such trust, or willfully suffers any other person so to do, commits ‘criminal breach of trust’.” Dowry Cases invariably have the component of ‘Criminal Breach of Trust’ relating to misappropriation of property. In case, the State relies upon the fiction of misappropriation, then the other party should have a right to know the details of property reflected in IT Returns which is alleged to be misappropriated.

19. That, Section 6(2) of the Act clearly states that the Applicant shall not be required to give any reason for requesting the information

From the paragraph 7 of the attached CIC judgment (Appeal : No. CIC/LS/A/2010/001044DS)

7. The conviction and thrust with which the Appellant had pursued his case and made his submission explaining the reasons for which he needs the information are plausible. But, however unfortunate as it may seem, the noise of motivation behind seeking the information falls upon deaf ears as far as the Act is concerned. Section 6(2) of the Act clearly states that the Applicant shall not be required to give any reason for requesting the information. Thus, the Act does not aim to judge the motivation or the reason behind seeking certain information, as each applicant may have a different line of reasoning, each one being equally passionate and emotionally driven.

20 Please also read and honour the below judgment of the APEX court of India that has been given in the case of “Arnesh Kumar Vs State of Bihar, in CRIMINAL APPEAL NO.1277 OF 2014 (@SPECIAL LEAVE PETITION (CRL.) No.9127 of 2013)” On 2nd July 2014.

There is phenomenal increase in matrimonial disputes in recent years. The institution of marriage is greatly revered in this country. Section 498-A of the IPC was introduced with avowed object to combat the menace of harassment to a woman at the hands of her husband and his relatives. The fact that Section 498-A is a cognizable and non-bailable offence has lent it a dubious place of pride amongst the provisions that are used as weapons rather than shield by disgruntled wives. The simplest way to harass is to get the husband and his relatives arrested under this provision. In a quite number of cases, bed-ridden grand-fathers and grand-mothers of the husbands, their sisters living abroad for decades are arrested. “Crime in India 2012 Statistics” published by National Crime Records Bureau, Ministry of Home Affairs shows arrest of 1,97,762 persons all over India during the year 2012 for offence under Section 498-A of the IPC, 9.4% more than the year 2011. Nearly a quarter of those arrested under this provision in 2012 were women i.e. 47,951 which depicts that mothers and sisters of the husbands were liberally included in their arrest net. Its share is 6% out of the total persons arrested under the crimes committed under Indian Penal Code. It accounts for 4.5% of total crimes committed under different sections of penal code, more than any other crimes excepting theft and hurt. The rate of charge-sheeting in cases under Section 498A, IPC is as high as 93.6%, while the conviction rate is only 15%, which is lowest across all heads. As many as 3,72,706 cases are pending trial of which on current estimate, nearly 3,17,000 are likely to result in acquittal.

Check Important Link

Joint Affidavit

BEFORE HON’NLE COURT OF JUDICIAL MAGISTRATE FIRST CLASS, PUNE AT PUNE.

Divorce Petition No. _______/2014

XYZA XXXX TTTT Petitioner -1

V/s

XXXX LLLLLL TTTT Petitioner -2

APPLICATION FOR DIVORCE BY HUSBAND AND WIFE U/S 13-B OF HMA 1955

The Humble petition of the Joint Petitioner being Petitioner no. 1 and the Petitioner No.2 herein MOST RESPECTFULLY SHEWETH :-

PRAYER: –

WHEREFORE, the both petitioners in above matter most respectfully prays that this Hon’ble court under the circumstances pray for a decree of dissolution of marriage by mutual consent under section 13B of the Hindu Marriage Act 1955..

Any other order in the circumstances of the case may also be passed.

Place: …………………. (Signature of the Petitioner 1)

Date: …………………..

Place: …………………. (Signature of the Petitioner 2)

Date: …………………..

Verification

I, Miss / Mrs. _______, Age:__ years, R/at: Flat no ________________________________ Pune 411033. do hereby verify that the contents from paras 1 to 9 are correct and true to the best of my knowledge and personal belief, faith and as per my instructions. The above contents have been read over and explained to me in Marthi / Hindi and I have understood the same. Hence I have signed hereunder on this ___ ________________ at Pune.

(Signature) Petitioner 1

Verification

I, Mr. _______________, Age:____ years, R/at: Flat no ____________________________, Pune- 411 033. do hereby verify that the contents from paras 1 to 9 are correct and true to the best of my knowledge and personal belief, faith and as per my instructions. The above contents have been read over and explained to me in Marthi/ Hindi and I have understood the same. Hence I have signed hereunder on this ___ ________________ at Pune.

(Signature) Petitioner 2

Check Important Link

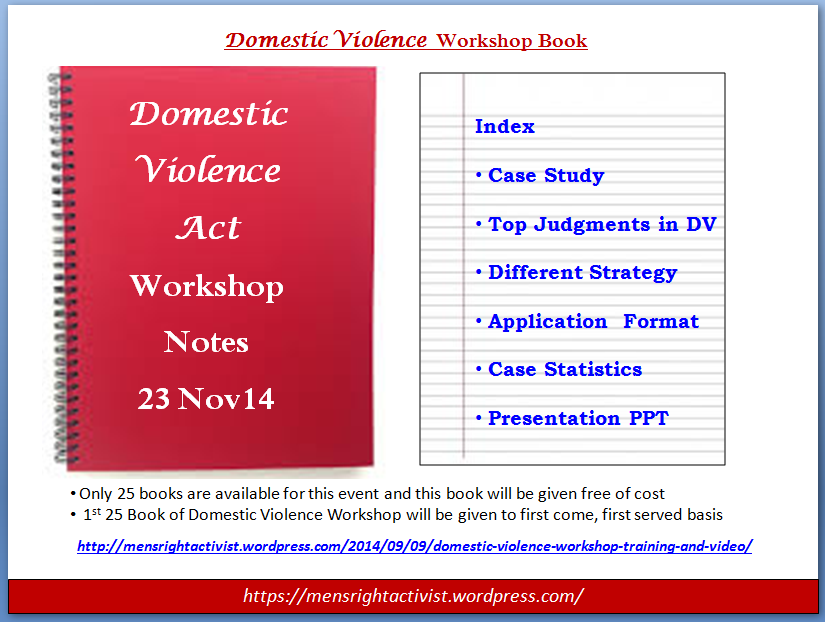

Free Domestic Violence Workshop, Training and Video

No Registration cost……, No Entry Free……., Workshop is free of cost…………,

Registration

Please send the following info to

Name/ Mobile number / Email id / Location / Case

Check Important Link

This WordPress.com site is the bee's knees